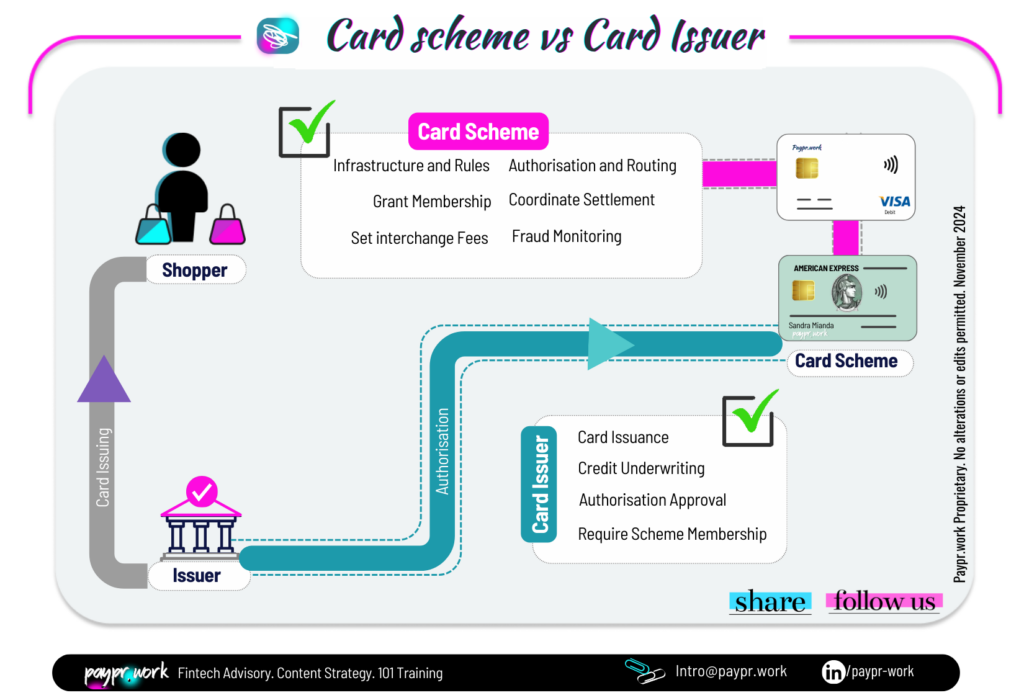

Global card schemes like Visa and Mastercard set the processing rules, but they don’t actually issue cards. In contrast, American Express and Discover Financial Services play on both sides. They control both the network and issue cards. This integrated approach can often be a source of confusion in the industry.

As I have illustrated in a previous post, the global payment landscape relies on complex interactions between various entities. What is interesting is the dynamic shift, whereby the boundaries between traditional payment roles are changing as more players, beyond financial institutions, take on multiple functions to adapt to new market demands. In this context, let’s look at some core differences between a card scheme and an issuer.

A card scheme typically acts as a facilitator, establishing the network for the transaction to flow between cardholders, merchants, and banks. On the other hand, a card issuer is the institution (i.e. bank, Fintech) that provides the cards directly to the consumers. Their functions can be summarised as follows:

𝐂𝐚𝐫𝐝 𝐒𝐜𝐡𝐞𝐦𝐞𝐬

✅ What they do:

◾ Set network rules and standards for the payment infrastructure

◾ Grant different levels of membership to financial institutions (i.e. direct issuing, acquiring capabilities)

◾Enable transactions authorisation and routing

◾ Set interchange fees between issuers and acquirers

◾ Fraud monitoring at the network level

◾ Coordinate the funds settlement between issuers and acquirers

❌ What they don’t typically do:

◾ Issue payment cards directly to consumers

◾ Manage individual card programmes

◾ Handle direct cardholder relationships

◾ Hold or move the funds themselves between issuers and acquirers

𝐂𝐚𝐫𝐝 𝐈𝐬𝐬𝐮𝐞𝐫𝐬

✅ What they do:

◾ Issue payment cards to consumers

◾ Manage cardholder accounts and transactions

◾ Underwrite credit and risk management

◾ Manage card programmes (e.g. rewards, loyalty)

◾ Oversee fraud detection for their own cardholders

◾ Require membership from a scheme or sponsorship (i.e. issuing rights)

❌ What they don’t do:

◾ Set the interchange fees or network rules

◾ Operate the underlying network

◾ Facilitate settlement between acquirers and merchants

American Express and Diners operate as closed-loop networks, acting as both issuer and acquirer, while fully managing the cardholder and merchant relationships.

👉🏽#Paymentexperts, any perspectives to share on #issuers vs #cardschemes?

—

𝑾𝒐𝒏𝒅𝒆𝒓 𝒘𝒉𝒐 𝒘𝒆 𝒂𝒓𝒆?

𝘞𝘦 𝘢𝘳𝘦 𝘢 𝘵𝘦𝘢𝘮 𝘰𝘧 𝘗𝘢𝘺𝘮𝘦𝘯𝘵𝘴 𝘚𝘵𝘳𝘢𝘵𝘦𝘨𝘪𝘴𝘵𝘴 𝘣𝘭𝘦𝘯𝘥𝘪𝘯𝘨 𝘰𝘶𝘳 𝘪𝘯𝘥𝘶𝘴𝘵𝘳𝘺 𝘦𝘹𝘱𝘦𝘳𝘵𝘪𝘴𝘦 𝘸𝘪𝘵𝘩 𝘢 𝘤𝘳𝘦𝘢𝘵𝘪𝘷𝘦 𝘢𝘱𝘱𝘳𝘰𝘢𝘤𝘩 𝘵𝘰 𝘢𝘴𝘴𝘪𝘴𝘵 𝘰𝘶𝘳 𝘤𝘭𝘪𝘦𝘯𝘵𝘴 𝘵𝘩𝘳𝘰𝘶𝘨𝘩 𝘊𝘰𝘯𝘴𝘶𝘭𝘵𝘪𝘯𝘨, 𝘚𝘵𝘳𝘢𝘵𝘦𝘨𝘺, 𝘙𝘦𝘴𝘦𝘢𝘳𝘤𝘩 𝘢𝘯𝘥 𝘛𝘩𝘰𝘶𝘨𝘩𝘵 𝘓𝘦𝘢𝘥𝘦𝘳𝘴𝘩𝘪𝘱 𝘱𝘳𝘰𝘫𝘦𝘤𝘵𝘴.

⏭ Follow Paypr.work [ˈpeɪpəwəːk]

⏭ Visit https://www.paypr.work/

⏭ Sign up to learn more: https://lnkd.in/dVXjGkzB

#paymentinfographics

#payprwork