A card transaction can happen online or offline…and no, we’re not talking about whether the transaction is processed on a website or physically in a store!

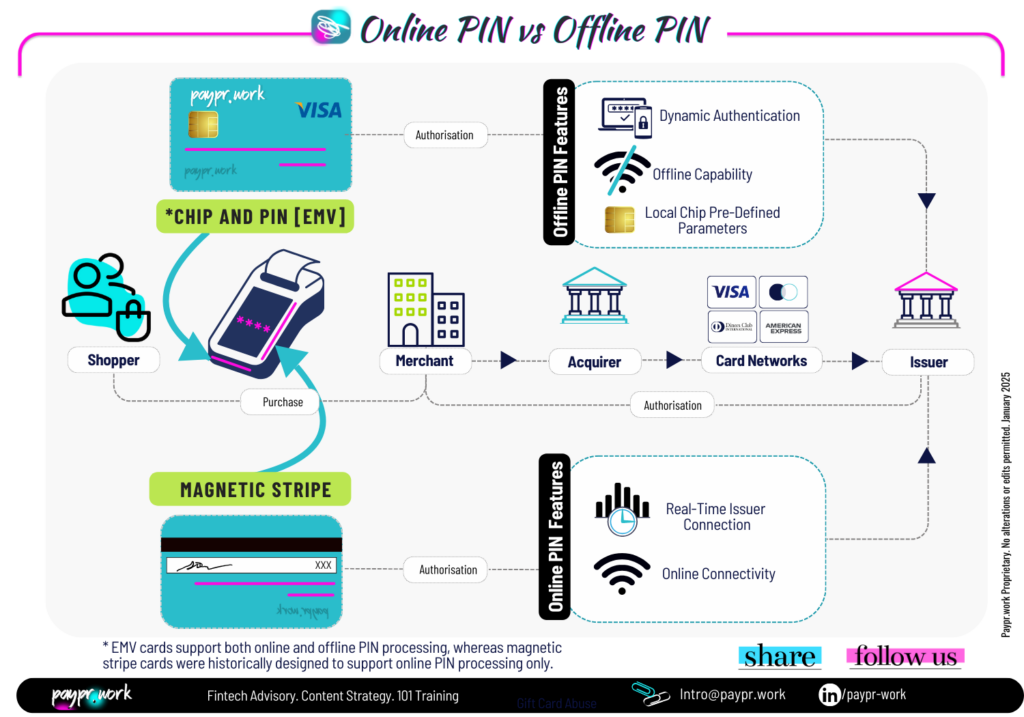

Back in the early days of card payments, cards were equipped with magnetic stripes. While groundbreaking at the time, these stripes stored static data, making them easy targets for fraudsters. Every transaction required a real-time connection to the issuer’s systems to authorise transactions. They require network connectivity during every payment to check for sufficient funds or credit and ensure transaction validity. For example, prepaid cards often fall into the “online-only” category, as their balances must be verified in real-time. A notorious country for online cards was the United States, which isn’t surprising considering magnetic stripe technology dominated there for decades.

Then came the game-changer with the EMV technology. Introduced in 1994, the chip brought dynamic data authentication and the ability to process transactions offline. This paved the way for hybrid systems where cards could seamlessly switch between online and offline authorisation modes based on the situation.

Offline PIN relies on the card’s embedded chip for local verification without requiring an immediate connection to the issuer. Instead, the card’s embedded chip or magnetic stripe stores data and uses predefined rules or limits to validate payments locally. Transactions are later reconciled with the issuer once connectivity is restored. Such uses are predominant in environments with limited or no internet connectivity.

On the other hand, Online PIN leverages real-time communication with the card issuer, offering enhanced security through centralised validation. Online PIN, in contrast, relies on real-time communication with the card issuer, offering a higher level of security through centralised validation. When the cardholder enters their PIN, the terminal encrypts it and transmits the data to the issuer’s server. The issuer checks the PIN against their secure database, validates the transaction, and provides immediate approval or decline. Because this method requires an active network connection, it is most commonly used in locations with reliable connectivity, such as ATMs, modern retail stores, and high-volume point-of-sale environments. Online PIN not only ensures more robust fraud prevention but also provides issuers with immediate visibility into transaction activity, enabling more effective risk management.

The contrast between these two methods reflects the interplay of technology, infrastructure, and security needs, demonstrating how payment systems adapt to different environments and levels of connectivity.

Today, modern payment cards incorporate both online and offline capabilities, delivering a mix of security and adaptability across any payment environment from chip-and-PIN to contactless.

👉🏽#Paymentexperts, any perspectives to add on the #card online vs offline #authorisation frameworks🎙️?

A card transaction can happen online or offline… Nothing new there… And no, we’re not talking about whether the transaction is processed on a website or physically in a store!

A card transaction can happen online or offline, nothing surprising there, but no, we’re not talking about whether it’s processed on a website or in a store!

A card transaction can happen online or offline, which isn’t surprising. But no, this isn’t about whether it’s processed on a website or in a store!

—

𝑾𝒐𝒏𝒅𝒆𝒓 𝒘𝒉𝒐 𝒘𝒆 𝒂𝒓𝒆?

𝘞𝘦 𝘢𝘳𝘦 𝘢 𝘵𝘦𝘢𝘮 𝘰𝘧 𝘗𝘢𝘺𝘮𝘦𝘯𝘵𝘴 𝘚𝘵𝘳𝘢𝘵𝘦𝘨𝘪𝘴𝘵𝘴 𝘣𝘭𝘦𝘯𝘥𝘪𝘯𝘨 𝘰𝘶𝘳 𝘪𝘯𝘥𝘶𝘴𝘵𝘳𝘺 𝘦𝘹𝘱𝘦𝘳𝘵𝘪𝘴𝘦 𝘸𝘪𝘵𝘩 𝘢 𝘤𝘳𝘦𝘢𝘵𝘪𝘷𝘦 𝘢𝘱𝘱𝘳𝘰𝘢𝘤𝘩 𝘵𝘰 𝘢𝘴𝘴𝘪𝘴𝘵 𝘰𝘶𝘳 𝘤𝘭𝘪𝘦𝘯𝘵𝘴 𝘵𝘩𝘳𝘰𝘶𝘨𝘩 𝘊𝘰𝘯𝘴𝘶𝘭𝘵𝘪𝘯𝘨, 𝘚𝘵𝘳𝘢𝘵𝘦𝘨𝘺, 𝘙𝘦𝘴𝘦𝘢𝘳𝘤𝘩 𝘢𝘯𝘥 𝘛𝘩𝘰𝘶𝘨𝘩𝘵 𝘓𝘦𝘢𝘥𝘦𝘳𝘴𝘩𝘪𝘱 𝘱𝘳𝘰𝘫𝘦𝘤𝘵𝘴.

𝑳𝒐𝒐𝒌𝒊𝒏𝒈 𝒇𝒐𝒓 𝒑𝒂𝒚𝒎𝒆𝒏𝒕 𝒍𝒆𝒂𝒓𝒏𝒊𝒏𝒈 𝒓𝒆𝒔𝒐𝒖𝒓𝒄𝒆?

◼️ Sign up to our unique Payment Assets Library here: https://lnkd.in/dVXjGkzB

◼️Follow Paypr.work [ˈpeɪpəwəːk] for more hashtag

#paymentinfographics #paymentinsights