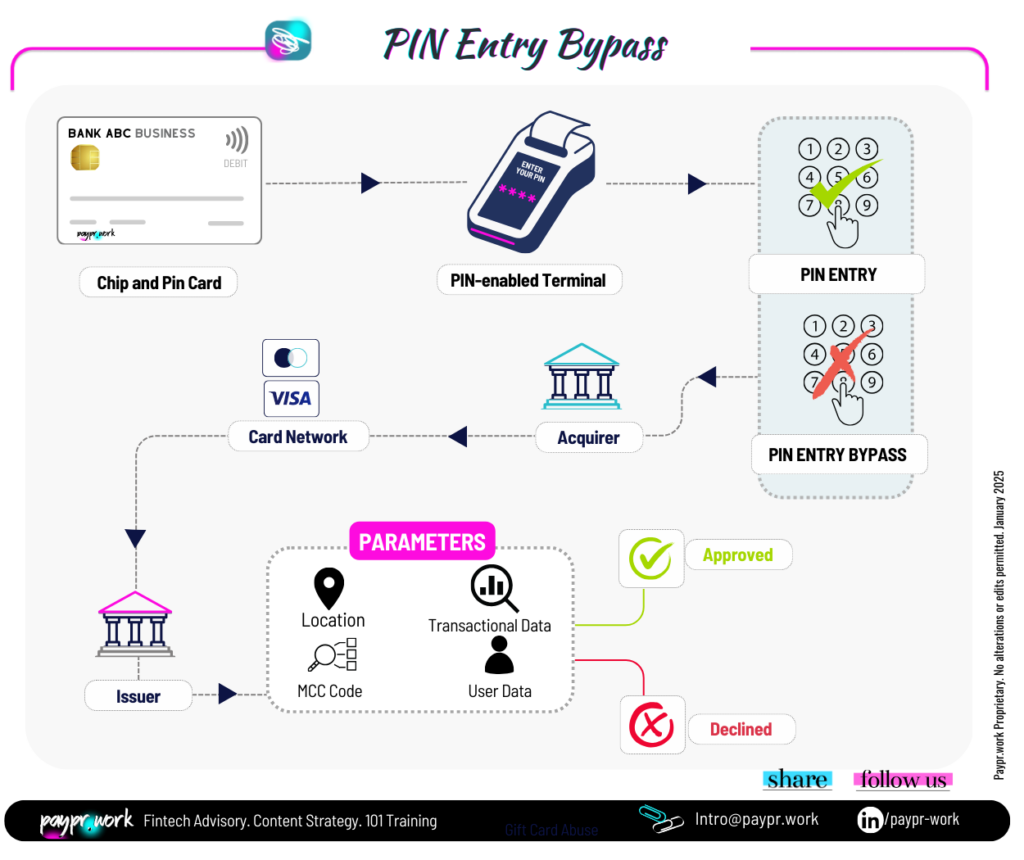

Continuing on the topic of PIN authentication there is another area worth diving into that fundamentally adds vulnerabilities to the card ecosystem… namely a process called PIN entry bypass, whereby the requirement to enter the PIN during a card-present transaction is skipped.

PINs are a critical layer of authentication in F2F transactions in the same way that 3DS is in e-commerce transactions. It may therefore seem odd or even counterintuitive that there are instances where this safeguard can be circumvented!

Essentially, in order for a terminal to prompt for a PIN when a customer uses an EMV card (chip and pin card), both the terminal and the card must be configured to allow the PIN entry. There are different scenarios why a POS terminal may not prompt for a PIN entry:

◾The terminal is not set up with the functionality

◾The card used does not support chip and PIN

◾The terminal supports the PIN entry bypass option

The guidelines around this PIN bypass process are defined in the EMV specifications. When a customer bypasses the PIN, it triggers a transaction indicator informing the issuer. This process, of course, bears some important considerations around liability and fraud exposure for the parties involved.

Whilst the EMV migration is a global mandate, a PIN entry bypass has historically been implemented in markets 𝐨𝐧𝐥𝐲 on a temporary basis (e.g. during a migration transition). In the US, however, where I first encountered this, it’s not uncommon to see a PIN bypass option on POS terminals. Card swiping and signature-based verification are also more widely used there compared to other markets.

Card issuers adopt different approaches to PIN bypass, e.g.:

◾Issuers may provide a grace period at the cardholder level, during which transactions can proceed without the PIN entry. After this period, the PIN will be required, or the transaction will be declined.

◾Some issuers use a risk-scoring model that evaluates factors such as the transaction location, Merchant Category Code (MCC), card type, and more to decide whether to allow PIN bypass.

◾While this process supports merchant routing choices, it comes with potential downsides such as issuer declines, lost sales, and increased exposure to fraud.

👉🏽#Paymentexperts, any perspectives to add on #PINbypass ?

—

𝑾𝒐𝒏𝒅𝒆𝒓 𝒘𝒉𝒐 𝒘𝒆 𝒂𝒓𝒆?

𝘞𝘦 𝘢𝘳𝘦 𝘢 𝘵𝘦𝘢𝘮 𝘰𝘧 𝘗𝘢𝘺𝘮𝘦𝘯𝘵𝘴 𝘚𝘵𝘳𝘢𝘵𝘦𝘨𝘪𝘴𝘵𝘴 𝘣𝘭𝘦𝘯𝘥𝘪𝘯𝘨 𝘰𝘶𝘳 𝘪𝘯𝘥𝘶𝘴𝘵𝘳𝘺 𝘦𝘹𝘱𝘦𝘳𝘵𝘪𝘴𝘦 𝘸𝘪𝘵𝘩 𝘢 𝘤𝘳𝘦𝘢𝘵𝘪𝘷𝘦 𝘢𝘱𝘱𝘳𝘰𝘢𝘤𝘩 𝘵𝘰 𝘢𝘴𝘴𝘪𝘴𝘵 𝘰𝘶𝘳 𝘤𝘭𝘪𝘦𝘯𝘵𝘴 𝘵𝘩𝘳𝘰𝘶𝘨𝘩 𝘊𝘰𝘯𝘴𝘶𝘭𝘵𝘪𝘯𝘨, 𝘚𝘵𝘳𝘢𝘵𝘦𝘨𝘺, 𝘙𝘦𝘴𝘦𝘢𝘳𝘤𝘩 𝘢𝘯𝘥 𝘛𝘩𝘰𝘶𝘨𝘩𝘵 𝘓𝘦𝘢𝘥𝘦𝘳𝘴𝘩𝘪𝘱 𝘱𝘳𝘰𝘫𝘦𝘤𝘵𝘴.

𝑳𝒐𝒐𝒌𝒊𝒏𝒈 𝒇𝒐𝒓 𝒑𝒂𝒚𝒎𝒆𝒏𝒕 𝒍𝒆𝒂𝒓𝒏𝒊𝒏𝒈 𝒓𝒆𝒔𝒐𝒖𝒓𝒄𝒆?

◼️ Sign up to our unique Payment Assets Library here: https://lnkd.in/dVXjGkzB

◼️Follow Paypr.work [ˈpeɪpəwəːk] for more hashtag#paymentinfographics

hashtag#paymentinsights

Paypr.work blends payment knowledge and custom research into a simplified yet insightful narration. Our narratives feature visually engaging designs that break down both fundamental and complex payment jargons into bite-sized, repetitive micro-concepts to promote better comprehension and retention.

Sign up for a Paypr.work Premium Membership to exclusively access all of our payment resources, including our full articles, industry insights, ecosystem maps, reports, videos, and our unique library of bespoke infographics.

Don’t miss out— sign up to learn payments in a captivating way!

You have provided so much light and knowledge in a fascinating world. You definitely bring the fun to Fintech like no one else and actually know what you are talking about! Thanks goodness for you😁!

Vice President Global Product Expansion, Shift4

Impressive, congratulations Sandra and Team Paypr.work. The detail in each of your 100+ infographics is outstanding and showcases your expertise well… Continued success for this remarkable work!

LinkedIn Strategist | Digital Transformation Leader

Host of Heads Talk

Your diagrams have the ability to explain the most complicated of topics in way that can be understood by anyone. Not many people have the ability to create self-explanatory visuals, so keep doing your magic 🔥🔥🔥!

CEO & Co Founder of CLOWD9

Your content is so informative, accurate, and fabulously presented in infographics that always attract great attention. Your visuals naturally spark strong engagement regardless of the LinkedIn algorithms !

B2B Marketing, Marqeta

The depth of Paypr.work knowledge and skill sets are truly impressive. Their ability to combine deep industry expertise with well-depicted visual is pretty unique. I strongly recommend Sandra and Paypr.work !

Director EMEA Payment Solutions, Marriott International

👏👏 👏👏 👏👏 I always love your content and in fact, I am so happy for all of us in the industry… we’re lucky to have you sharing your payment wisdom with us 🤓… thank you! Keep up the great work.

Strategic Accounts Director, Truelayer | Payments and Fintech Geek

Merci Sandra pour ta facilité à vulgariser le paiement via de simples dessins, qui me surprendront toujours. Pour ceux qui ne connaissent pas son travail, je vous invite à suivre Paypr.work [ˈpeɪpəwəːk]!

Product Manager Paiement, Maisons du Monde

Your enthusiasm and ability to simplify Payments is so refreshing and literally shines through! Sandra and her team research, write content and create some stunning infographics for the payments industry….

Chief Operations Officer, Clowd9

Keep up the good work and know that your hard work and dedication is so inspiring for all of us. You are truly doing an incredible job and your consistent efforts don’t go unnoticed.

Chief Community Officer, NORBr | Redefining Payment Infrastructure | Linkedin Top Voice

Your posts are a masterclass in how payments have evolved from a basic utility to a strategic asset. Your ability to simplify this complexity and provide strategic direction along with implementation support is so invaluable. The clarity and depth you provide are exactly what this fast-evolving industry needs.

Chief Commercial and Operations Officer, Soffid

The mechanics of all things payment are a black box for most industry stakeholders. With the help of their well researched and designed infographics, Sandra and her team at Papr.work demystify complex flows and create awareness about the factors that play a role in the end to end processes.

Paul van Alfen | Managing Director Managing, Up in the Air - Travel Payment Consultancy

Your Paypr.work subscription gets you full access to all Paypr.work content in 1 place including: our weekly new payments articles, our infographic blog, exclusive discounts on all the services that Paypr.work has to offer and the opportunity to collaborate on free infographic to promote your knowledge/value proposition and more. The content is for personal use and cannot be copied, reproduced, redistributed, altered, modified, shared publicly or with third-party nor can derivatives of the work be created. The user may share content that is available through the free blog access subject to crediting Paypr.work with the attributions.