The concept of a card floor limit has played a significant role in the evolution of payment processing. Traditionally, a floor limit represented the maximum transaction amount a merchant could accept without requiring authorization from the card issuer. This practice was essential in offline transactions, helping businesses process small-value payments quickly without needing electronic approval. However, as digital payment systems have become more sophisticated, real-time transaction authorization has largely rendered traditional floor limits obsolete.

In the past, floor limits were determined based on factors such as merchant category, transaction environment, and risk profiles. For example, a retail store might have a higher floor limit than a gas station due to varying fraud risks. These limits were enforced to balance transaction efficiency with fraud prevention, ensuring that small purchases could be processed smoothly while larger transactions required verification.

However, with the widespread adoption of EMV chip technology, contactless payments, and real-time authorization systems, card networks and issuers now approve nearly all transactions instantly. This shift has minimized the relevance of traditional floor limits, as card payments are now validated for security, available funds, and fraud risks in real time.

Despite their diminishing role, floor limits still exist in specific scenarios, such as:

As digital payments continue to surge, the dominance of card networks like Visa and Mastercard highlights the importance of real-time processing. In fiscal year 2024, Visa reported a total payment volume of $15.7 trillion, processing 233.8 billion transactions on its networks. Meanwhile, Mastercard’s net revenues saw a 14% increase, reaching $7.5 billion in the fourth quarter, driven by a 13% rise in payment network revenues and 20% growth in cross-border volumes. These figures underscore how real-time authorization and fraud monitoring have become the backbone of modern payment networks, reducing the necessity of floor limits in most cases.

As payments become increasingly digital and instant, floor limits will continue to fade in importance. However, they may persist in niche use cases where instant authorization is impractical. With the rise of AI-driven fraud detection, biometric authentication, and real-time risk analysis, merchants and consumers alike can enjoy faster, more secure transactions without the constraints of outdated floor limit policies.

In today’s payment ecosystem, real-time authorization has replaced the need for static floor limits, ensuring a seamless and secure experience for businesses and consumers alike.

#didyouknow

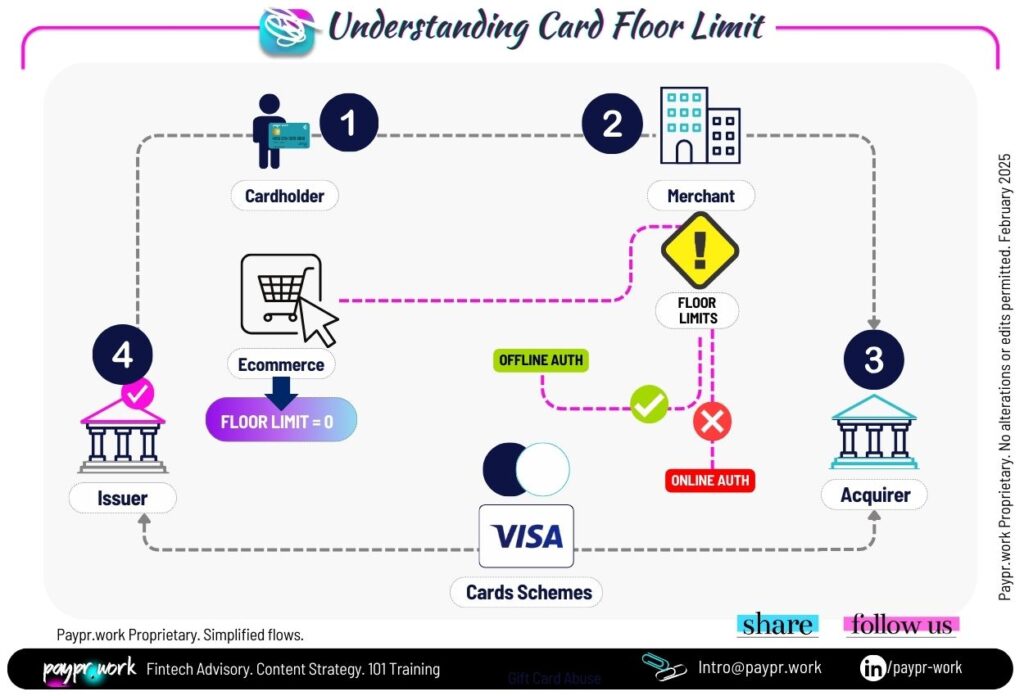

◼️From a credit risk perspective, ecommerce transactions are deemed high risk and as a result will pretty much always have a zero-floor limit. This means that all ecommerce transactions are sent for authorisation regardless of the amount.

◼️The floorlimit term dates from back in the days, when cashiers used to authorise payments over the phone, calling the bank literally from the sales floor when a customer passed their limit… hence the term.

◼️ From a credit risk perspective, eCommerce transactions are deemed high risk and, as a result, will pretty much always have a zero-floor limit. This means that all eCommerce transactions are sent for authorization regardless of the amount.

◼️ The floor limit term dates back to the days when cashiers had to authorize payments over the phone, literally calling the bank from the sales floor if a customer exceeded their limit. This process led to the term “floor limit.”

◼️ Some merchants, such as airlines and hotels, may have different floor limits depending on the service. A hotel might set a higher floor limit for room charges, but still require real-time authorization for additional purchases, such as at the minibar or restaurant.

◼️ Floor limits can play a role in disaster recovery scenarios. When payment networks experience outages, some merchants have contingency plans that allow for offline transactions up to a predefined limit before authorization becomes necessary.

◼️ Some countries have regulatory-imposed floor limits for specific transaction types.