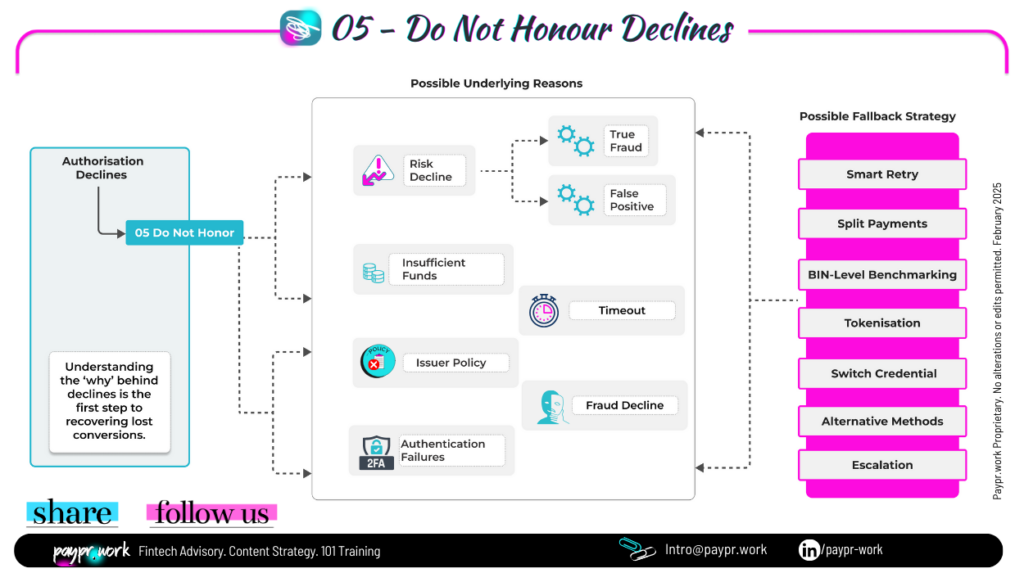

Let’s talk about the ambiguity of decline codes… because about 30–40% of transaction declines are still reportedly categorised as “Do Not Honor.”

Pinning down a definitive average for card decline rates is tricky. Decline percentages can differ significantly depending on the industry, vertical, and the card networks or processors in use. Some sectors experience far higher decline rates than others, and in many cases, consistent reporting is lacking altogether. Historically, the ecosystem relied on broad-stroke categories to communicate transaction outcomes. It worked, until it didn’t. As payments grew more global, more complex, and more digital, so did the need for granularity.

Still, the question remains… when a transaction returns a “Do Not Honor” code, it creates confusion and opens a black box of possible reasons. Fraud? Insufficient funds? Issuer logic? Or something else entirely? Timeout, data mismatch, or bad routing logic can all cause this generic decline. Issuers could return a more specific code, but often don’t. Sometimes it’s to protect against giving fraudsters too much insight, sometimes it’s just down to legacy systems or lack of issuer-side transparency.

The lack of clarity has real consequences for merchants. When you don’t know why a transaction failed, you can’t make informed decisions whether to retry, reroute, or let it go. That uncertainty leads to lost revenue, frustrated customers, and poor checkout conversion. And in today’s environment of rising false declines, clarity isn’t a nice-to-have, it’s mission-critical.

Decline response codes are defined and standardised by the card schemes (like Visa and Mastercard) as part of the ISO 8583 messaging framework. This framework sets the structure and meaning of the codes globally. However, how those codes are applied in practice and whether they are used with consistency and granularity depends largely on the issuer.

Issuers decide which decline codes to send based on their internal decisioning systems, which may include:

While the card schemes define the set of decline response codes under the ISO 8583 messaging standard, it is ultimately up to the issuer to determine how and when each code is applied. As a result, similar transaction scenarios may be classified differently depending on the issuer’s internal policies, risk models, or system configurations. For example, one issuer may return a “Do Not Honor” (code 05) response, while another may return a more specific “Fraud/Security” (code 83) for the same type of decline.

But declines are packed with insight—if it’s clear what to look for.

With the right mapping, benchmarking, and context, decline codes can do far more than simply signal a failed transaction. They can help merchants proactively optimise performance across their payments stack.

By clustering decline codes and mapping them to specific steps in the payment journey, you can identify where drop-offs are happening, whether it’s a failed authentication, a timeout, or a misconfigured routing rule. These friction points often go unnoticed until the data reveals a pattern.

Not all issuers behave the same. Some decline disproportionately, apply stricter fraud controls, or have technical quirks. By analysing decline rates at the BIN or issuer level, merchants can spot underperformers and work with acquirers or schemes to troubleshoot or adjust routing strategies.

Armed with data, merchants can do more than just react—they can act. Whether it’s fine-tuning retries, updating authentication flows, or implementing smart routing, a clearer view of decline behaviour opens the door to higher approval rates and better checkout experiences.

A Shift Toward Specificity

Now, the card schemes are stepping up. Mastercard has introduced Decline Reason Code 83 (Fraud/Security) replacing the overly broad “Do Not Honor” (Code 05) in some CNP scenarios. Visa is also introducing new Category 2 response codes in April 2025, offering issuers a way to signal more precise reasons like “Transaction blocked by issuer” or “Blocked by cardholder.” These changes may seem minor, but they mark a broader shift toward transparency and shared accountability and that matters more than ever when every decline could mean a lost customer.

Why This Matters Now

Retailers and digital platforms are investing heavily in reducing friction at checkout. But even the best checkout flow can’t solve the problem if a transaction is mysteriously declined with no explanation. According to industry studies, as many as 1 in 5 declined transactions are false positives, cases where legitimate customers are blocked by over-aggressive fraud systems or misconfigured issuer logic.

This is particularly painful for subscription models, digital wallets, and cross-border merchants, where retry logic and smart routing depend on interpreting decline signals properly.

With these new codes from Mastercard and Visa, there’s hope for greater transparency, better decisioning, and ultimately, higher acceptance rates. But only if the ecosystem is prepared. With more granularity, you can build smarter retry strategies, avoid triggering unnecessary security flags, and reduce abandonment.

These updates are a step in the right direction, but decline code ambiguity is still far from solved. The more the industry demands clarity, the faster things will evolve.

Most fallback strategies hinge on one thing: visibility.

Smart retry logic, network tokenisation, and dynamic routing only work when you understand why a transaction failed. Without that signal, you’re flying blind—and blind retries waste time, add cost, and frustrate customers.

Some merchants address this by building internal logic—delaying and retrying based on BIN-level patterns or issuer behaviour. Others rely on providers offering adaptive retry mechanisms: rerouting through alternate acquirers, tweaking transaction metadata, or shifting from stored credentials to real-time entry.

But even the smartest retry strategy is only as good as the signals feeding it.

That’s why it matters that schemes like Visa and Mastercard are finally refining decline codes.

More context = better routing = higher approval rates.

The bottom line? Getting a second chance at a transaction starts with knowing why the first one failed.

#paymentexperts, any perspectives to share🎤?

—

𝑾𝒐𝒏𝒅𝒆𝒓 𝒘𝒉𝒐 𝒘𝒆 𝒂𝒓𝒆? 𝘞𝘦 𝘢𝘳𝘦 𝘢 𝘵𝘦𝘢𝘮 𝘰𝘧 𝘗𝘢𝘺𝘮𝘦𝘯𝘵𝘴 𝘚𝘵𝘳𝘢𝘵𝘦𝘨𝘪𝘴𝘵𝘴 𝘣𝘭𝘦𝘯𝘥𝘪𝘯𝘨 𝘰𝘶𝘳 𝘪𝘯𝘥𝘶𝘴𝘵𝘳𝘺 𝘦𝘹𝘱𝘦𝘳𝘵𝘪𝘴𝘦 𝘸𝘪𝘵𝘩 𝘢 𝘤𝘳𝘦𝘢𝘵𝘪𝘷𝘦 𝘢𝘱𝘱𝘳𝘰𝘢𝘤𝘩 𝘵𝘰 𝘢𝘴𝘴𝘪𝘴𝘵 𝘰𝘶𝘳 𝘤𝘭𝘪𝘦𝘯𝘵𝘴 𝘵𝘩𝘳𝘰𝘶𝘨𝘩 𝘊𝘰𝘯𝘴𝘶𝘭𝘵𝘪𝘯𝘨, 𝘚𝘵𝘳𝘢𝘵𝘦𝘨𝘺, 𝘙𝘦𝘴𝘦𝘢𝘳𝘤𝘩 𝘢𝘯𝘥 𝘛𝘩𝘰𝘶𝘨𝘩𝘵 𝘓𝘦𝘢𝘥𝘦𝘳𝘴𝘩𝘪𝘱 𝘱𝘳𝘰𝘫𝘦𝘤𝘵𝘴.

🔘 Need help with your payment or product strategy? Let’s talk: intro@ppw-editor

🔘 Looking for Payments learning resources, check out our unique hub: https://lnkd.in/dVXjGkz

🔘 Follow Paypr.work [ˈpeɪpəwəːk] for more weekly #paymentinsights #paymentinfographics