It may sound strange today, but in the early 2000s, when platforms and marketplaces like eBay and Amazon were starting to reshape how commerce worked, the payments infrastructure was simply not built for this kind of scale or flexibility. The industry was still primarily built for traditional, one-merchant-at-a-time models, where a single business accepted payment and fulfilled the order.

Most acquirers saw these aggregated new setup as too complex and too risky. The idea of one platform collecting payments on behalf of hundreds or even thousands of sellers raised all sorts of questions:

◾Who owns the funds

◾Who gets paid when

◾Who’s liable if something goes wrong

PayPal, which became the default for eBay sellers, was one of the few solutions to emerge with a workaround, effectively acting as an early aggregator, managing funds and risk on behalf of both sides.

Later in the decade, companies like Airbnb and Uber pushed the model further, forcing the industry to rethink aggregation, not as a workaround, but as a core strategy for enabling platform payments at scale.

▪️ Ownership of funds

▪️ Timing and flow of payouts

▪️ Liability in the event of fraud or disputes

PayPal stepped in early, acting as a de facto aggregator for eBay sellers—managing payments and risk on behalf of both sides. But this was the exception, not the rule.

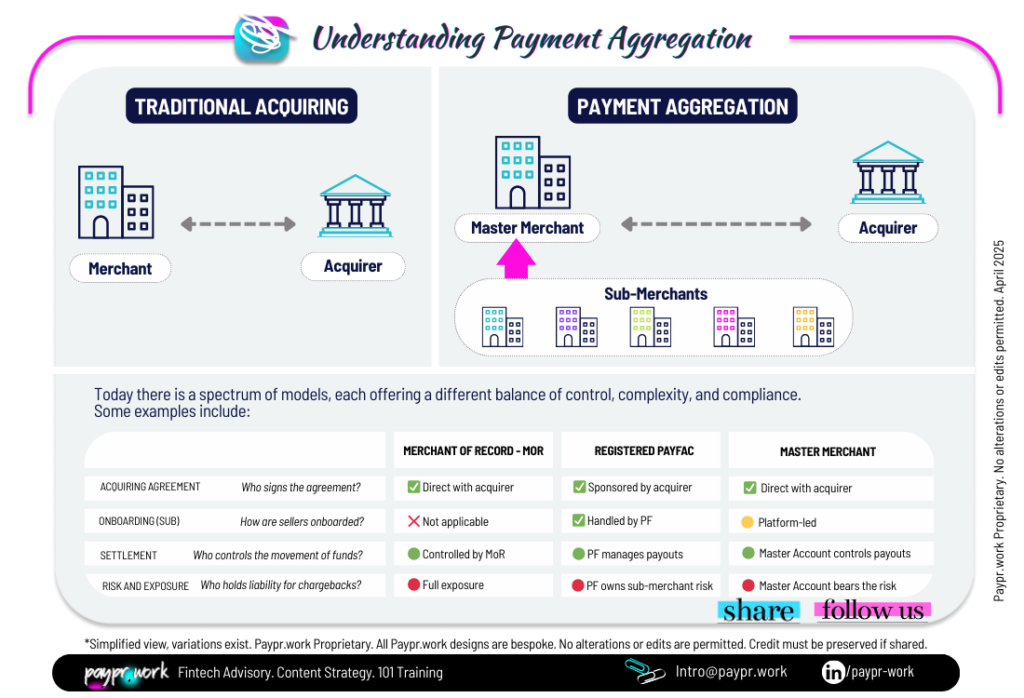

To fill the gap, many businesses adopted the Master Merchant model, common in sectors like travel, adult content, and gaming. It allowed platforms to process payments centrally on behalf of multiple sellers. But it also introduced regulatory and operational challenges—particularly around transparency, chargebacks, and AML enforcement.

Over time, pressure from schemes and regulators led to stricter requirements:

In parallel, wallets emerged as an alternative route—offering a layer of abstraction where direct card acquiring was too complex or commercially unviable.

The shift came later in the decade.

As the platform economy matured, players like Airbnb, Uber, Stripe Connect, Square, and Adyen for Platforms redefined aggregation—turning it from a workaround into a scalable, programmable infrastructure.

What changed?

▪️ API-first onboarding

▪️ Built-in KYC/KYB

▪️ Real-time sub-merchant creation

▪️ Risk controls baked into the stack

Aggregation was no longer a compliance challenge—it became a core strategy for platform enablement.

Where does that leave us today?

Modern platforms now choose between:

Master Merchant model – maximum control, high complexity

Registered PayFac – scalable but operationally intensive

Managed PayFac solution – Stripe, Adyen, Checkout.com, etc.

#paymentexperts, any perspectives to share on the #aggregation or #payfac models🎤?

—

𝑾𝒐𝒏𝒅𝒆𝒓 𝒘𝒉𝒐 𝒘𝒆 𝒂𝒓𝒆? 𝘞𝘦 𝘢𝘳𝘦 𝘢 𝘵𝘦𝘢𝘮 𝘰𝘧 𝘗𝘢𝘺𝘮𝘦𝘯𝘵𝘴 𝘚𝘵𝘳𝘢𝘵𝘦𝘨𝘪𝘴𝘵𝘴 𝘣𝘭𝘦𝘯𝘥𝘪𝘯𝘨 𝘰𝘶𝘳 𝘪𝘯𝘥𝘶𝘴𝘵𝘳𝘺 𝘦𝘹𝘱𝘦𝘳𝘵𝘪𝘴𝘦 𝘸𝘪𝘵𝘩 𝘢 𝘤𝘳𝘦𝘢𝘵𝘪𝘷𝘦 𝘢𝘱𝘱𝘳𝘰𝘢𝘤𝘩 𝘵𝘰 𝘢𝘴𝘴𝘪𝘴𝘵 𝘰𝘶𝘳 𝘤𝘭𝘪𝘦𝘯𝘵𝘴 𝘵𝘩𝘳𝘰𝘶𝘨𝘩 𝘊𝘰𝘯𝘴𝘶𝘭𝘵𝘪𝘯𝘨, 𝘚𝘵𝘳𝘢𝘵𝘦𝘨𝘺, 𝘙𝘦𝘴𝘦𝘢𝘳𝘤𝘩 𝘢𝘯𝘥 𝘛𝘩𝘰𝘶𝘨𝘩𝘵 𝘓𝘦𝘢𝘥𝘦𝘳𝘴𝘩𝘪𝘱 𝘱𝘳𝘰𝘫𝘦𝘤𝘵𝘴.

🔘 Need help with your payment or product strategy? Let’s talk: intro@paypr.work

🔘 Looking for Payments learning resources, check out our unique hub: https://lnkd.in/dVXjGkz

🔘 Follow Paypr.work [ˈpeɪpəwəːk] for more weekly #paymentinsights #paymentinfographics #payprwork