#didyouknow

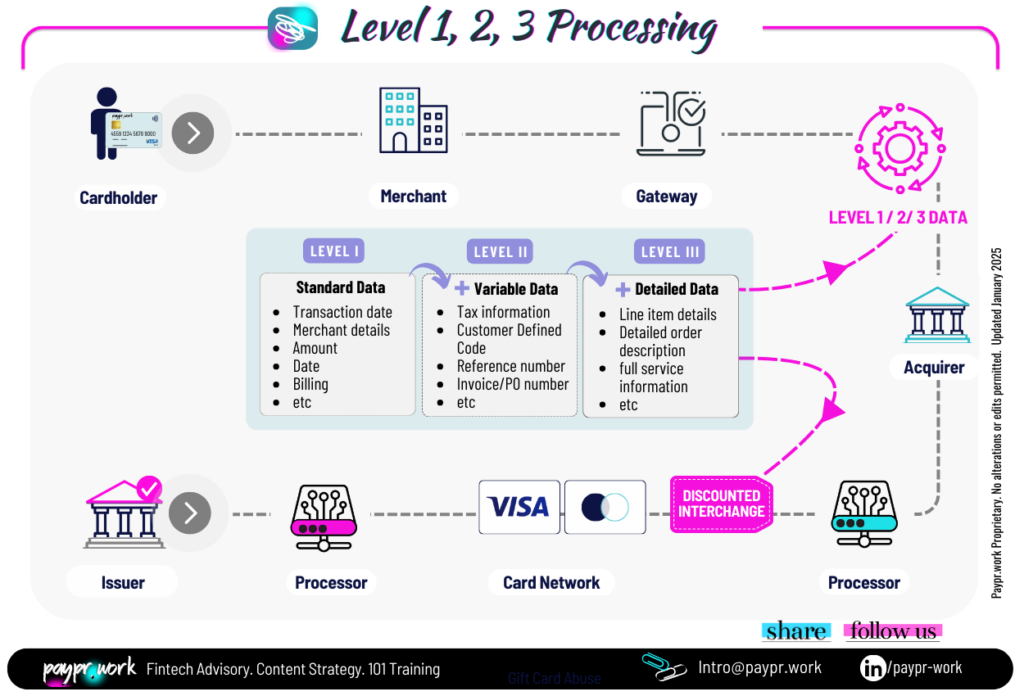

Card processing fits into three levels, namely Level 1, Level 2 and Level 3. Each level is defined by the amount of information that is required or passed to complete a payment, with Level 1 having the lowest requirements and potentially the highest cost structure.

◾𝐋𝐞𝐯𝐞𝐥 𝟏 data are the standard transaction details that pretty much every gateway/PSP captures, typically for B2C transactions (i.e. date, amount etc).

◾ 𝐋𝐞𝐯𝐞𝐥 𝟐 data refers to more variable transaction information typically designed to support B2B payment flows.

◾ 𝐋𝐞𝐯𝐞𝐥 𝟑 requires the capture of specific line item data that defines 𝐰𝐡𝐚𝐭 is being purchased, 𝐡𝐨𝐰 the sales takes place, 𝐰𝐡𝐨 is involved in the transaction, and 𝐰𝐡𝐞𝐧 it takes place.

𝐒𝐨 𝐰𝐡𝐲 𝐝𝐨𝐞𝐬 𝐋𝟐 𝐚𝐧𝐝 𝐋𝟑 𝐝𝐚𝐭𝐚 𝐦𝐚𝐭𝐭𝐞𝐫?

◾Card transactions submitted with Level 2 and Level 3 card data can obtain lower interchange rates and provide merchants with a lower processing cost. They are predominantly used in B2B, government, airlines, and industries handling large-ticket items. In airlines, Level 2/3 data is key for calculating and managing risk exposure.

◾Visa and Mastercard offer specific interchange programs for Large Ticket items (LTI), which determine qualifying transactions subject to scheme approval.

◾The exact discount depends on the level of the transaction and, in some cases, the actual amount of the transaction. Savings can range between 0.2% to 1%+ on the interchange.

◾The interchange fees make up 70%-85% of the card processing fees, hence why level 2/3 processing can be so vital.

For merchants, benefiting from a level 2 or level 3 transaction discount requires layers of additional data to be captured/added at the time of a transaction and to be formatted according to the schemes rules.

However, it is key to note that:

◾ Not all cards are enabled for L2 / L3.

◾ Not all gateways/PSPs are equipped with the technology to capture and convert L2 and L3 datafields.

◾Not all processors and acquirers support reduced interchange for large ticket level 3 transactions.

So in essence, the more data points are correctly collected, the easier it is for every player in the chain of payments to assess risks, optimise the fees structure, facilitate quicker and more secure payment approvals.