Settlement cycles are changing. Where T+1 (next-day) or T+2 settlements were once standard, several markets are now moving toward T+0, namely same-day settlement.

This shift is being driven by a mix of infrastructure upgrades, regulatory initiatives, and market demands for greater liquidity and reduced risk. India, for example, has introduced optional T+0 settlement for its top 500 listed stocks. In retail payments, real-time payment systems like PIX (Brazil), UPI (India), and SEPA Instant (EU) have set new expectations around speed and availability of funds.

But this isn’t just about speed. It’s about redefining how presentment fits into the broader payment flow.

Presentment is a foundational—but often overlooked—component of the payment lifecycle. It refers to the merchant’s formal submission of a transaction to their acquiring bank for settlement. In other words: authorisation secures the intention, but presentment triggers the actual movement of fun

Despite its centrality, presentment often receives limited attention outside of payment operations teams. But with industry-wide shifts toward faster settlement, particularly the global momentum toward T+0 (same-day) processing, this once-back-office step is fast becoming a strategic focal point.

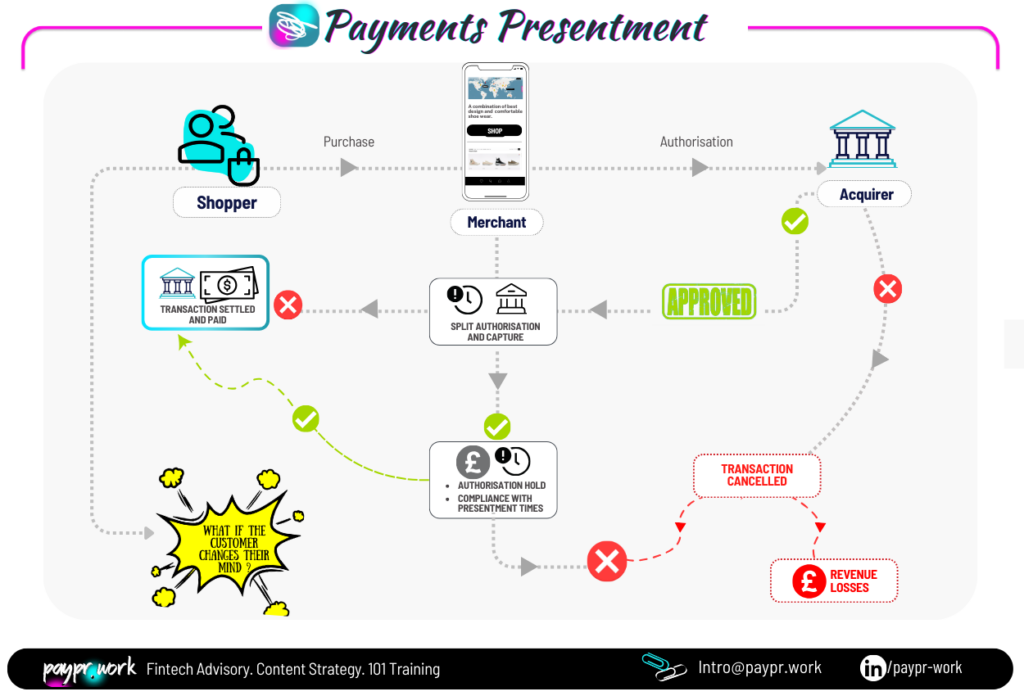

Let’s look at the traditional card payment flow:

1️⃣ Authorisation / Pre-authorisation

2️⃣ Batching

3️⃣ Clearing / Presentment / Capture

4️⃣ Funding / Settlement

Following an approved authorisation, the merchant places a temporary hold on the customer’s account. This hold is not a charge—it simply reserves the funds and provides conditional assurance. To transform that hold into payment, the merchant must present the transaction for settlement—typically within a scheme-defined timeframe, known as the presentment window.

If the merchant fails to present within that window, several risks arise:

Presentment, therefore, is not just procedural—it’s financially consequential.

Globally, the settlement landscape is evolving. Several markets are moving from T+1 (next-day settlement) toward T+0, where transactions are settled on the same day they are executed.

India has taken the lead, recently rolling out optional T+0 settlement for its top 500 stocks. Meanwhile, conversations in Europe suggest a possible leapfrog directly to T+0 for certain instruments. These moves reflect a broader push for efficiency, liquidity, and reduced counterparty risk.

But what does this mean for presentment?

In a T+0 environment, the authorisation-presentment lag must be compressed—or eliminated entirely. For merchants and payment processors, this shift brings both opportunity and pressure:

In this new paradigm, presentment can no longer be a deferred task. It must be treated as part of a continuous, tightly managed payment lifecycle.

Certain sectors will continue to rely on pre-authorisation and delayed capture models—though they too will need to adapt if T+0 becomes standard:

🏨 Hospitality – Card authorised at check-in; presentment post-checkout

🚗 Car rental – Hold at booking or pickup; capture on vehicle return

🛍️ Ecommerce – Pre-auth at checkout; presentment after order is shipped

These use cases are valid, but increasingly depend on clear coordination between operational and payments teams to avoid reversals and customer confusion.

T+0 introduces a structural shift that compresses the overall payment lifecycle, and presentment is one of the most affected stages. Therefore, getting the presentment windows right in this context means rethinking:

As the industry embraces faster settlement cycles, presentment is no longer a hidden middle step—it’s a front-line issue that can unlock or undermine financial performance. Whether you operate in traditional retail, ecommerce, or platform-based ecosystems, getting presentment right—at the right time—is essential.