The payment industry is a fascinating sector that never ceases to evolve and innovate🚀. From the advent of mobile payments and digital wallets to the rise of blockchain technology and cryptocurrencies, there is an abundance of technological developments revolutionising the way payments operate.

When a transaction is initiated, there are primarily two types of process that happen:

Front-end process, namely the user experience at the point of purchase be it on a POS, in-App or online that capture the transactions details and route it through to the payment ecosystem to gain authorisation. This is will be the object of a post next week.

Back-end process, namely the the core of the technology that enable the money movement between the customer, the merchants and their respective banks. This where distinctive functions are assumed by acquirer, acquirer-processor or pure processors. The issuer and the processor can be the same entity, but they are often not. In fact, this division between issuer and issuer processor is increasingly common.

➡️An Acquiring Bank, also known as card acquirers, are financial institutions, whose primary role is to enable merchants to accept payments. They handle the authorization, processing, and settlement of transactions, ensuring that funds from cardholders’ accounts are transferred to the merchants’ accounts. They serves as a centralised hub for handling various aspects of the payment flow and work directly with merchants, providing support, underwriting merchant accounts, and managing risk.

➡️Traditionally, banks have been the primary players in the acquiring space, owning the infrastructure, expertise, and regulatory framework to handle payment processing.

➡️ As a result, a lot of the technology that processes billions of online card payments every year is actually quite outdated.

➡️ However, with the rise of fintech and third-party payment processors, non-bank entities have entered the acquiring market. These entities offer innovative payment solutions and cater to the evolving needs of merchants and consumers by leverage next-gen technology, rich analytics capabilities to enhance the payment process and partnerships with banks or card networks to provide acquiring services, all without being a traditional bank themselves.

➡️Non-bank acquirers bring diversity and competition to the payment industry. They often specialize in specific niches or offer tailored solutions for specific industries, such as e-commerce or mobile payments. These companies focus on providing efficient, user-friendly experiences for merchants and customers, often leveraging advanced technology and analytics capabilities to enhance the payment process.

➡️Acquirers also offer additional services beyond payment processing, such as risk management, chargeback handling, and merchant account management.

➡️It’s important to note that while non-bank acquirers may not have the same regulatory oversight as banks, they still need to comply with industry regulations and security standards to ensure the integrity and security of transactions. They work closely with card networks, financial institutions, and regulatory bodies to meet these requirements and maintain the trust of merchants and consumers.

➡️A Payments Processor is the infrastructure that handles the technical aspects of processing transactions.

➡️Their primary function is to securely transmit transaction data and facilitate the authorization, clearing, and settlement of payments. They do not directly engage with merchants but collaborate with acquirers to enable secure and efficient payment transactions.

➡️ Payment processors have direct connections to major card networks (such as Visa or Mastercard) and banks, allowing them to facilitate transactions across different payment methods. They handle the technical infrastructure required for secure data transmission, encryption, and fraud prevention.

➡️Fintech-led processors are a game changer in the processing space. As a result of their tech-first approach they bring agility, new features, quicker deployment and enhanced security, ultimately benefiting merchants and cardholders.

➡️Whilst major acquirers have their own in-house processing capabilities, others collaborate with third-party payment processors to handle the technical aspects of payment processing. This partnership allows acquirers to leverage the expertise and infrastructure of dedicated processors while focusing on their core role of merchant relationship management and additional value-added services.

There can be some overlap between the roles of acquirers and payments processors, however their key differences lie in their primary areas of focus. Acquirers primarily focus on managing the financial aspects of the payment process, and the assuming risk, whilst the payments processors specialise in the technical aspects of payment processing, including data transmission, security, and integration with various payment networks. There are various reasons why an acquirer may not want to assume a processor role, for example as a result of i.e.:

➡️Specialization. Some acquirers specialize in certain types of businesses, such as retail or hospitality. They may not have the expertise or resources to also act as a processor.

➡️Cost. It can be expensive to operate as both an acquirer and a processor. Some acquirers choose to outsource the processing function to a third-party in order to save money.

➡️Regulation. There are different regulatory requirements for acquirers and processors. Acquirer are subject to stringent regulatory requirements and oversight. They must comply with financial regulations, undergo audits, and adhere to industry standards to ensure the security and integrity of payment processing. Payments processors also have their own set of regulatory obligations, but they are typically subject to fewer regulatory requirements compared to acquirers. Their focus is primarily on maintaining secure technology infrastructure and complying with data protection regulations. Some acquirers may not want to deal with the additional compliance burden of also being a processor.

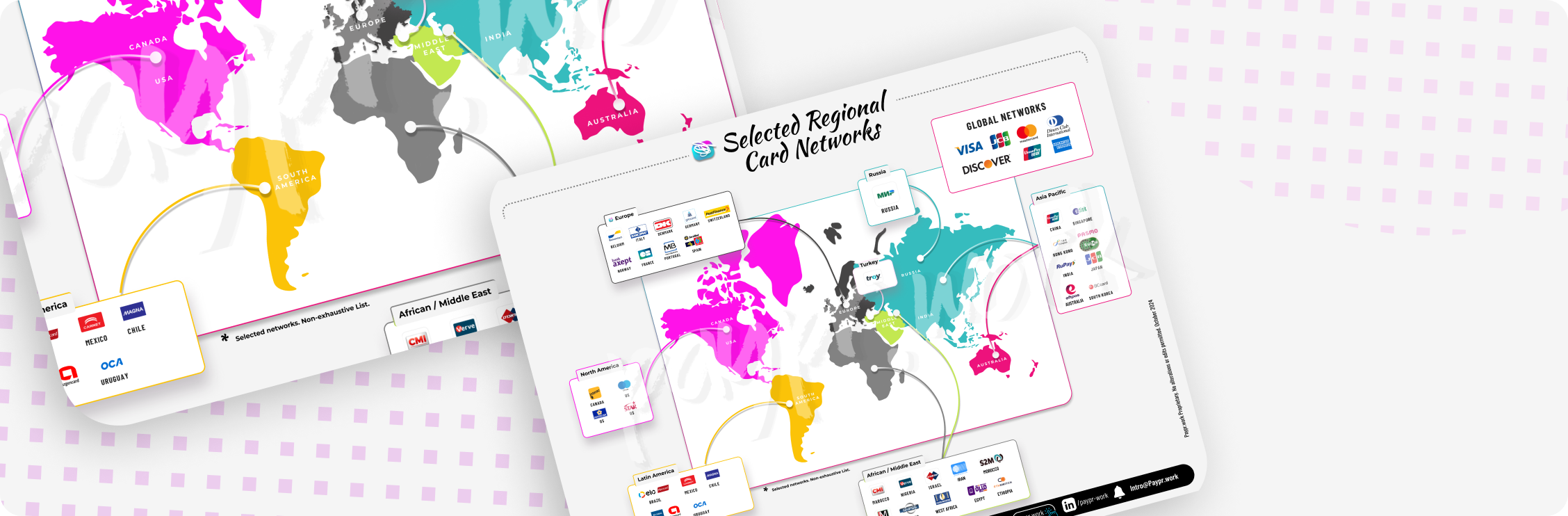

The landscape of acquirers and processors is vast and constantly evolving, with mergers, acquisitions, new entrants shaping the industry, and with numerous companies operating in crossed roles. Additionally, there are regional and country-specific acquirers and processors that may be prominent within specific markets. Nevertheless, here is a selective list of players onto that field.