Fraud has always been a persistent challenge, but in recent years, it has transformed from isolated incidents into a full-blown global crisis, posing a significant threat to the trust and security of the payment ecosystem. What began as localised schemes has grown into a sophisticated, globalised issue, exploiting every innovation in payments and commerce. Today, fraud operates on a global scale, exploiting vulnerabilities in digital platforms, payment systems, and regulatory gaps

Ironically, the very advancements that have propelled the financial systems forward, namely technology, globalisation, and complex infrastructures, have also fuelled the evolution of fraud into a sophisticated and pervasive issue. The evolution reflects the increasing complexity and wider challenge posed by these threats.

Fraudsters consistently adapt to exploit every wave of innovation. From counterfeiting to phishing, and now AI-driven fraud and synthetic identities, their methods grow more advanced with each passing year. According to Ravelin Technology’s 2024 Fraud Report, 57% of businesses reported a rise in fraud attempts over the past year, with machine learning and synthetic identities becoming major tools in fraudsters’ arsenals.

Merchant Fraud Risks Vary Significantly

Merchant fraud risks can vary widely depending on factors such as industry, transaction channels, customer demographics, and geographic location. For instance, e-commerce businesses often face high rates of card-not-present (CNP) fraud, accounting for nearly 85% of all payment fraud losses in 2023. Meanwhile, brick-and-mortar retailers might grapple with return fraud or theft of gift card balances, which reportedly costs the retail industry over $24 billion annually.

Tailored fraud prevention strategies are critical to addressing these unique risks. A one-size-fits-all approach often fails to account for specific patterns, such as unusual transaction behaviors, regional fraud trends, or emerging attack vectors like synthetic identity fraud—estimated to cost the U.S. economy $4.5 billion annually. Similarly, businesses with recurring revenue models face higher risks from account takeover (ATO) attacks, which surged by 67% in 2023, as fraudsters exploited weak credential security and automation tools.

Effective prevention requires:

Without this alignment, businesses risk relying on generic solutions that may miss subtle, targeted threats. For example, a fraud tool optimized for retail transactions might not effectively mitigate the risks faced by subscription services or cross-border payment platforms. The result? Higher operational costs, damaged customer trust, and increased fraud losses, which reached a staggering $41 billion globally in 2023.

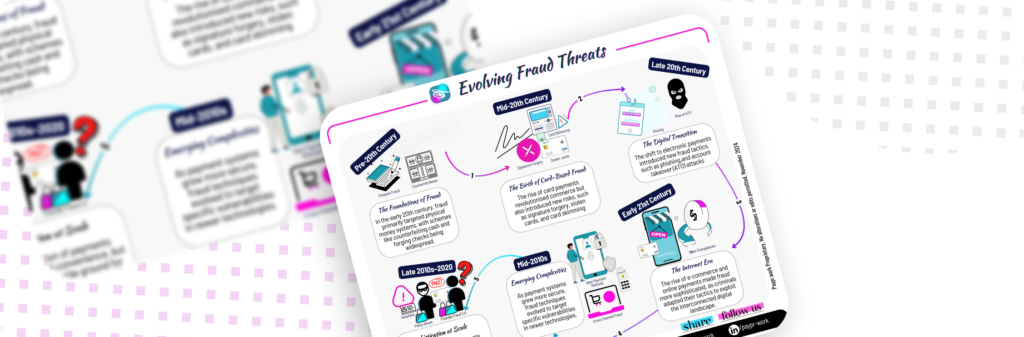

The Sophistication of Fraud, How did we get Here…

The roots of fraud lie in the earliest financial systems, where physical currency and paper-based transactions dominated commerce.

Though primitive by modern standards, these early fraud techniques laid the groundwork for more elaborate schemes in the future.

Mid-20th Century: The Birth of Card-Based Fraud

The advent of payment cards revolutionised commerce, but they also introduced new vulnerabilities for exploitation.

As the payment ecosystem expanded, fraudsters adapted, finding new ways to exploit these innovations.

Late 20th Century: The Digital Transition

The digital revolution brought a new wave of payment systems—and fraud techniques.

The digitalisation of payments offered speed and convenience, but it also created a fertile ground for increasingly sophisticated fraud.

Early 21st Century: The Internet Era

With the explosion of e-commerce and online payments, fraud became more dynamic, adapting to the connected world.

The internet era democratised commerce, but it also allowed fraudsters to operate on an unprecedented scale.

Mid-2010s: Emerging Complexities

As payment systems grew more secure, fraud techniques evolved to target specific vulnerabilities in newer technologies.

These new methods underscored the adaptability of fraud in response to technological progress.

Late 2010s–2020s: Sophistication at Scale

The digital payments landscape became more advanced—and so did fraud.

In this era, fraudsters began leveraging the same tools—AI, machine learning, and automation—that financial institutions use to prevent them.

The evolution of fraud reflects its adaptability and persistence. As payment systems become more advanced, fraudsters innovate, finding new ways to exploit vulnerabilities. For the payment industry, this ongoing arms race underscores the need for vigilance, collaboration, and investment in cutting-edge technologies to stay ahead.

Combating fraud is not just about reacting to new threats—it’s about building systems that anticipate and prevent them. By placing trust and security at the core of the payment ecosystem, the industry can continue to foster innovation while safeguarding the integrity of global commerce.